Energy Storage: Are We There Yet?

Everyone recognizes the Energizer Bunny, the marketing icon for Energizer Batteries in North America. He keeps going and going and going. And that’s exactly what we want from an energy storage solution.

In the power industry, we are largely concerned about bulk energy storage and we want a technology that can be cycled (charged and discharged) efficiently, has a long use duration, is efficient, cheap and the list goes on. And did I mention, the ideal technology also must have a manageable footprint? Power industry executives claim that mastery of energy storage is the “golden fleece” for the industry and once we get there, it will revolutionize the business. So, the question is: Are we there yet? The answer, as you may have guessed, depends upon who you ask, and of course, there are some caveats.

There is no question that the domestic energy storage market is red hot. According to the U.S. Energy Storage Markets YIR report for 2015, deployments were up 243%. But at a utility-scale system price ranging from $700/kWh to $1,200/kWh, where does storage make sense? Here is where the caveats come in.

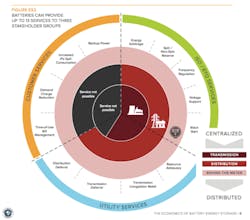

According to a study prepared by the Rocky Mountain Institute (RMI), energy storage makes sense when multiple functions can be achieved with an installation (caveat number one). Multiple functions should translate to multiple sources of revenue or avoided cost credits. RMI provided an excellent graphic in its study “The Economics of Battery Energy Storage” to illustrate the many services provided by energy storage depending on its location on the electrical system.

A great testimonial about achieving higher value from a solar installation through the use of battery storage was contributed by Don Harrod, administrator for the Village of Minster, Ohio, and appears in the April issue of T&D World (see Solar Meets Energy Storage).

So here’s my dilemma: If storage is the “golden fleece” for the industry, why are some storage projects failing and others, like pumped storage, which still constitutes greater than 90% of all energy storage capacity, becoming uneconomic for the owners? Well, it may be those pesky caveats again. Caveat number one is (at current storage costs) multiple sources of revenue are needed. Some traditional storage projects relied largely on energy arbitrage and that just doesn’t work today. While pumped storage projects should be able to capture spinning reserve, regulation and other ancillary service revenues, they also have huge O&M expenses and require a lot of real estate. Other storage projects have failed because the markets were not designed to allow them to recover all of the benefits they were capable of providing. This situation is caveat number two in a nutshell. The storage application and or the market must be designed to allow cost recovery on the investment.

As depicted in the RMI graphic, central storage stations may defer investment and provide multiple services. If a facility is not in a location that has a developed market for those attributes and/or the investment does not receive regulatory recognition for those benefits, cost recovery will not be possible. RMI believes that many behind-the-meter storage projects, including battery storage which is perhaps twice the cost of flywheel and pumped storage, are net positive at today’s costs when the projects can use all the benefits from their installation on-site (offset demand charges, backup power supply, etc.) or recoup revenue from services supplied to the grid.

The rub is market anatomy, rates and regulatory policies have a huge impact on storage technology viability and they have not kept pace with storage technology advancements. Distributed energy resources with storage often times cannot participate in ancillary service markets. Front-of-the meter resources also may be unable to obtain market recognition for certain services if there is no developed market for them. Some states and regulators have recognized this shortfall and are acting. Initiatives in New York, New Jersey, Oregon, California and elsewhere are gaining momentum to remove energy storage barriers. Utilities and other stakeholders who have not joined this debate need to engage because the benefits of storage technology advancements for them and certainly for their customers will not be fully realized until the market regulatory and rate barriers to storage technology use are addressed. So to answer my own question, maybe were not quite there yet…what do you think?

About the Author

David Shadle

Grid Optimization Editor

Dave joined the T&D World team as the editor of the Grid Optimization Center of Excellence website in January 2016.

Dave is a power industry veteran with a history of leading environmental and development organizations, championing crucial projects, managing major acquisitions and implementing change. Dave is currently a principal at Power Advance, LLC, an independent consulting firm specializing in power project development, research and analysis, due diligence and valuation support. Dave is also a contributing consultant for Transmission & Distribution World. Prior to Power Advance, Dave held business and power project development positions with The Louis Berger Group, Iberdrola Renewables, FPL Energy and General Public Utilities. He is a graduate of Pennsylvania State University, the New Jersey Institute of Technology and Purdue University.